TL;DR

- MTD uses a points-based penalty system for late submissions.

- Each missed quarterly update = 1 penalty point.

- Once you reach the threshold, a £200 fine is issued.

- Further late submissions trigger additional £200 penalties.

- Points only reset after a sustained period of full compliance.

Introduction

Making Tax Digital isn’t just about quarterly submissions.

It’s about consistency.

From April 2026, sole traders and landlords within scope of Making Tax Digital must comply with strict reporting deadlines set by HM Revenue & Customs.

Miss one deadline?

You receive a penalty point.

Miss several?

You start paying fines.

Unlike the old Self Assessment regime — where penalties often escalated dramatically — MTD introduces a structured, accumulation-based system.

But don’t be misled.

Small delays compound quickly.

Here’s exactly how MTD penalties work for 2026/27.

Who Is Affected in 2026/27?

From 6 April 2026, MTD for Income Tax applies to:

- Sole traders earning £50,000+ gross income

- Landlords earning £50,000+ gross rental income

From April 2027, the threshold drops to £30,000.

If you fall within scope, quarterly deadlines are mandatory.

And so is the penalty system.

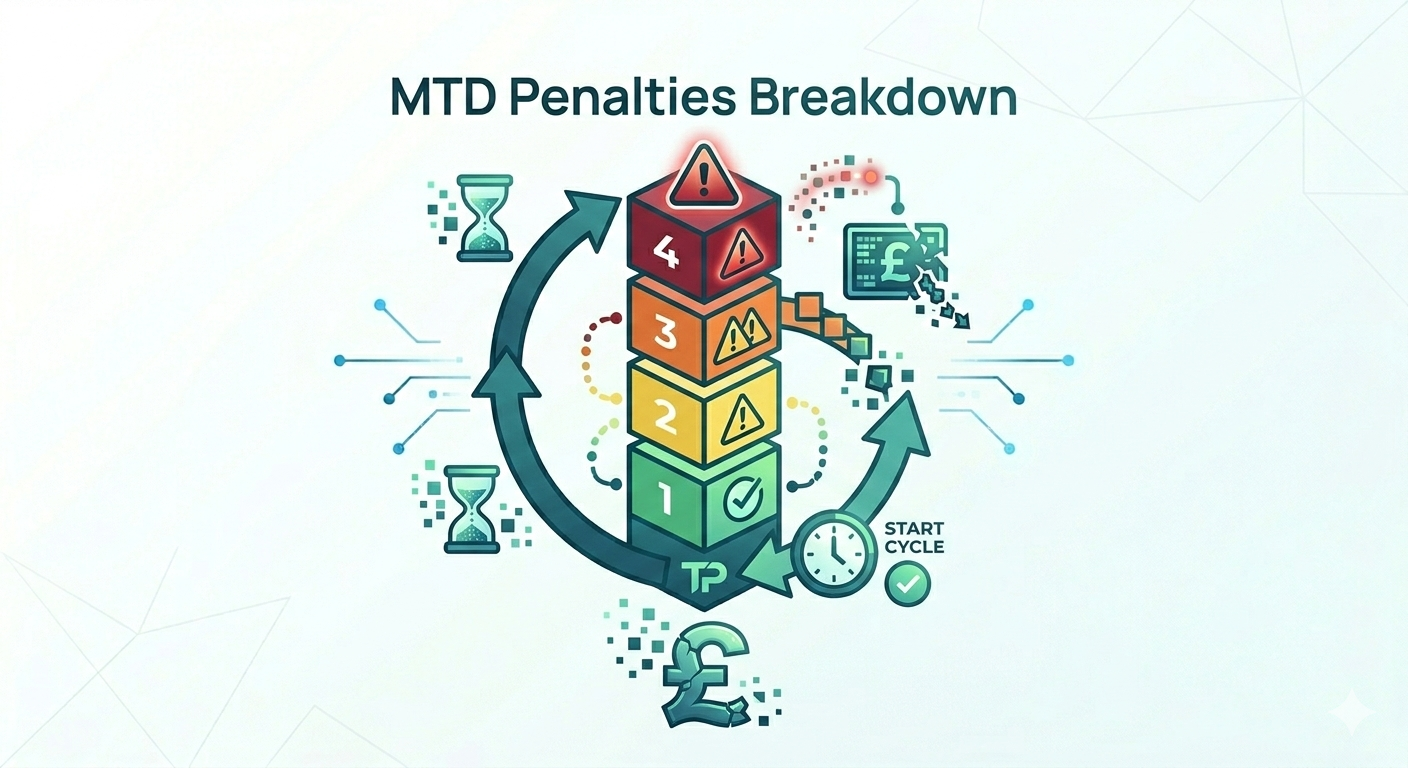

How the MTD Points System Works

Under MTD, late submissions earn penalty points instead of immediate fines.

For quarterly filers:

- 1 late submission = 1 penalty point

- Points accumulate

- Once you reach the threshold, a fine is triggered

For quarterly reporting, the points threshold is:

4 penalty points

At that point, a financial penalty applies.

This system encourages compliance without immediate punishment — but it does not forgive repeated lateness.

When Do Fines Apply?

Once you hit 4 points:

- A £200 fine is issued.

After reaching the threshold:

- Each additional late submission results in another £200 fine.

Points do not reset automatically after a fine.

You must complete a full compliance period.

Repeated lateness becomes expensive.

How Points Expire

Penalty points expire only when:

- You submit all required returns on time for a sustained compliance period, and

- You bring all outstanding submissions up to date.

For quarterly filers, the compliance period is typically:

12 months of on-time submissions.

If you miss another deadline during that period?

The clock resets.

Consistency matters.

What About Late Payment Penalties?

The points system applies to late submissions.

Late payment penalties are separate.

If tax is paid late:

- 15 days late → initial penalty

- 30 days late → additional penalty

- Ongoing daily interest accrues

The later the payment, the higher the cost.

Quarterly updates may not require payment — but the final declaration does.

Real-World Example

Let’s say a sole trader misses:

- Q1 deadline → 1 point

- Q2 deadline → 2 points

- Q3 deadline → 3 points

- Q4 deadline → 4 points → £200 fine

If they then miss the next quarter:

- Another £200 fine applies immediately

That’s £400 in fines within a short period.

All avoidable.

Common Misunderstandings

“It’s just one late submission.”

Yes — and that’s one point closer to a fine.

“Points disappear automatically.”

No. They require full compliance to expire.

“My accountant handles it.”

You are still legally responsible for compliance.

Delegation does not remove liability.

Key Takeaways

- MTD uses a points-based penalty system

- Quarterly filers receive a fine after 4 points

- Each additional late submission = £200 fine

- Points only expire after sustained compliance

- Late payment penalties are separate

- Delegating to an accountant does not remove responsibility

- Consistency prevents unnecessary fines

Final Thoughts

MTD penalties in 2026/27 are not designed to punish one-off mistakes.

They are designed to penalise patterns of non-compliance.

The system is predictable.

Transparent.

And avoidable.

Four late submissions may not sound dramatic.

But £200 fines — multiplied — add up quickly.

With five compliance events per year, discipline becomes critical.

Stay Compliant Before Penalties Start

If you’re unsure whether your systems are ready for quarterly submissions — or whether your business falls within the 2026/27 MTD scope — review your setup now and ensure you’re fully prepared before the first deadline passes.

FAQs

How many points trigger a fine?

Under Making Tax Digital for Income Tax, the number of penalty points that trigger a financial penalty depends on your submission frequency.

For most sole traders and landlords within MTD:

- You are a quarterly filer

- The penalty threshold is 4 points

This means:

- 1 missed submission = 1 point

- 4 points = £200 financial penalty

After you reach 4 points:

- Every further missed submission results in an additional £200 penalty

- You do not need to accumulate another 4 points to trigger the next fine

So practically, once you reach the threshold, the system becomes less forgiving.

Important detail:

Points are tracked separately per obligation. For example, quarterly updates and final declarations are part of the same MTD obligation — but VAT (if registered) operates independently under its own penalty record.

The key operational risk is this:

Under the old Self Assessment system, you had one annual filing deadline.

Under MTD, you have five filing events per year.

That increases exposure to points significantly if admin discipline is weak.

Do penalty points expire?

Do penalty points expire?

Yes — but not automatically and not quickly.

Penalty points remain active until you:

- Submit all outstanding returns, and

- Complete a defined compliance period with no further failures.

For quarterly filers, this compliance period is typically 12 months of on-time submissions.

Key implications:

- If you accumulate 3 points in year one and then miss another deadline early in year two, you immediately hit 4 points and trigger a fine.

- Points do not simply “drop off” after a few months.

- You must actively return to full compliance before they reset.

This means your first year under MTD (2026/27) is critical.

Poor habits in the first year can carry forward and create financial penalties in later years.

Can penalties be appealed?

Yes — but only where you can demonstrate a reasonable excuse, and you must provide evidence.

Examples HMRC may accept:

- Serious illness (with medical evidence)

- Bereavement close to the deadline

- Significant IT system failure outside your control

- Unforeseeable events (e.g. fire, flood)

Examples typically rejected:

- “I forgot”

- “I was too busy”

- Cash flow problems

- Reliance on an accountant without oversight

Important:

You must appeal within the stated timeframe after the penalty notice is issued. Appeals are not automatic and are not informal — they require a structured submission.

Even if you use accounting software such as:

- Xero

- QuickBooks

- FreeAgent

You remain legally responsible for compliance.

Software failure alone does not automatically remove liability unless you can prove it was genuinely outside your control.

Strategic Takeaway

The MTD penalty regime is not necessarily harsher than the old system.

But it is:

- More frequent

- More trackable

- Less forgiving of repeated minor failures

In 2026/27, operational discipline becomes as important as tax planning.

Compliance is no longer annual.

It is continuous.

Leave a Reply